The 24-Year-Old Selling NVIDIA: What ASX Investors Should Take From the Aschenbrenner Trade

By Dannika Warburton

In late 2024, a 24-year-old former OpenAI researcher walked into a meeting with a handful of Silicon Valley’s most successful founders, including Stripe’s Patrick and John Collison, Nat Friedman, and Daniel Gross. He had just published a 165-page essay titled Situational Awareness: The Decade Ahead. Most readers treated it as bold futurism. The room he was sitting in read it as a pitch deck.

The result was Situational Awareness LP, a hedge fund built around a single thesis: artificial general intelligence is arriving faster than the market is pricing, and the real money will be made not in the algorithms but in the physical infrastructure required to run them. By February 2026, the fund’s 13F filing disclosed US$5.52 billion in US equity exposure across 29 holdings, having grown from a US$254.8 million, six-holding filing in Q4 2024.

The fund manager is Leopold Aschenbrenner. He is now 25. And in his most recent quarterly filings, he has been quietly rotating out of the obvious chip plays and into something else entirely.

The trade

The Situational Awareness fund initiated a position in Bloom Energy during the fourth quarter of 2025, before Wall Street caught on. Aschenbrenner understood that training and running AI models would add to electricity demand at scales that existing power infrastructure simply could not handle. Bloom Energy’s solid-oxide fuel cells offer a clever workaround for powering data centres: on-site, modular power generation that can be deployed efficiently at hyperscale facilities, bypassing congested utilities and providing reliable baseload electricity around the clock.

Bloom Energy is now the fund’s single largest holding. The stock has run up 176% since the position was initiated. Around it sit positions in CoreWeave (AI cloud infrastructure), Cipher Mining, Core Scientific, IREN, and Applied Digital, all companies operating large, power-hungry computing facilities originally built for Bitcoin mining and increasingly being repurposed for AI workloads.

Public 13F filings disclose only long positions in US-listed stocks. Short positions, derivatives, and international investments remain hidden. Still, the portfolio suggests a clear thesis: the most valuable assets in the AI era may not be algorithms but electricity and computing power. Rather than betting primarily on the companies building AI models, Situational Awareness is betting that the real bottlenecks will be electricity generation and computing capacity.

The thesis is testable against very large, very current numbers.

Chart: Bloom Energy (BE) YTD performance – up 210% – showing the infrastructure rotation in action (Google Finance, as at 9 May 2026).

The capex backdrop

Microsoft, Alphabet, Meta, and Amazon are now expecting to invest up to US$725 billion in 2026, the majority of it on AI infrastructure: data centres, chips, and networking equipment. In 2024, the combined capex of the four biggest hyperscalers was just over US$200 billion. Two years later, it is on track to approach US$700 billion. If this is a climb, there is still no clear view of the summit.

The constraint is no longer money, it’s power. Microsoft has disclosed an US$80 billion backlog of Azure orders that cannot be fulfilled due to power constraints, and Meta has announced a 1GW data centre in Ohio and a Louisiana facility that could eventually scale to 5GW. Combined capital expenditures at Alphabet, Amazon, Meta, Microsoft, and Oracle have been growing at an average of 72% per year since the second quarter of 2023, and on current trajectory will reach US$770 billion in 2026.

The implication is straightforward. Capital is flowing into the AI buildout faster than the grid can absorb it. Everything that supplies the power, the cooling, and the copper underneath that buildout is part of the same trade.

The Australian read

The Aschenbrenner fund is US-listed and macro in scale, but the logic translates directly to the ASX, and Australian investors with exposure to the right resources stories are arguably better positioned than US capital to play it.

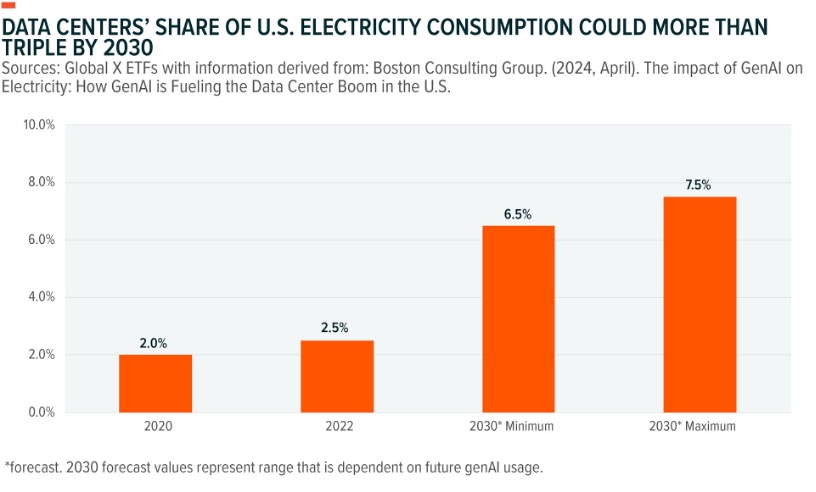

International Energy Agency executive director Dr Fatih Birol described Australia at the National Press Club this year as a potential “global resource rising star,” noting that the country’s combination of LNG, lithium, copper, cobalt, and uranium reserves places it at the centre of the energy transition and the rise of AI-driven infrastructure. A single medium-sized data centre can consume as much electricity as a town of 100,000 households.

The supply-demand picture for the inputs is structural. Global copper output projections indicate supply reaching only 29 million tonnes by 2035, substantially below the 35 million tonnes required under current demand scenarios. Citi is targeting copper to average US$12,000 per tonne by the second quarter of 2026, with bull-case scenarios extending materially higher should deficits persist. UBS’s 2026 copper price assumption sits at US$5.20 per pound, comfortably above consensus, reflecting confidence that supply constraints will outweigh any residual demand volatility.

Uranium tells a similar story. The uranium term price, which reflects the majority of uranium sales undertaken through long-term contracts between miners and utilities, sits at 18-year highs of around US$90/lb. Uranium was added back to the US Critical Minerals List by the US Geological Survey in November 2025, and the US Government and Westinghouse Electric’s owners have agreed to build at least US$80 billion worth of nuclear reactors. Growth in artificial intelligence data centres has driven an increase in US power demand for the first time in two decades.

For ASX-listed resource companies in copper, uranium, gas, and rare earths, the question is no longer whether AI demand is real. It is whether the equity story is positioned to capture the global capital that is actively rotating into these themes.

Why the Aschenbrenner trade matters for ASX directors

Three things stand out for boards and management of ASX-listed resource and energy companies watching this thesis play out.

The first is that a fund of this size, run by someone this close to the underlying technology, is rotating through the AI stack faster than most institutional capital can keep up with. The Situational Awareness fund went from a six-holding US$254.8 million book in Q4 2024 to a 29-holding US$5.52 billion book by February 2026. The pivots from semiconductors to power, and then to repurposed Bitcoin miners with AI hosting capacity, happened across consecutive quarters. Australian companies in the supply chain for these themes have a window to position narrative and disclosure with global investors who are still actively rebalancing.

The second is that the AI infrastructure thesis is multi-layered and not all layers are equally investable from Australia. Approximately 75% of aggregate hyperscaler capex in 2026 will fund AI infrastructure, representing roughly US$450 billion in AI-specific spending. The chip layer (NVIDIA, Broadcom, Intel) is overwhelmingly US and Asian. The model layer (OpenAI, Anthropic, Google) is mostly private or concentrated in the largest US listed names. Where Australia sits comfortably is in the foundational layer underneath everything else: the energy, the copper, the uranium, and the gas required to make the buildout physically possible. That is the layer Aschenbrenner is buying. ASX-listed companies in that layer should be telling that story to global capital, not just domestic retail.

The third is that a strong narrative is doing a lot of the work in this market. The Situational Awareness fund’s average multiple across its five largest positions is approximately 14x EV/Revenue, well above traditional value benchmarks. In a market trading on momentum and forward-looking narrative rather than backward-looking earnings, clean storytelling about exposure to structural demand is being rewarded. Australian companies with genuine exposure to AI infrastructure inputs that fail to articulate that exposure clearly are leaving capital on the table for those that do. We have written previously on why most ASX companies are targeting the wrong investors, and the same principle applies here. The capital is moving. The question is whether the companies in the right sectors are positioned to attract it.

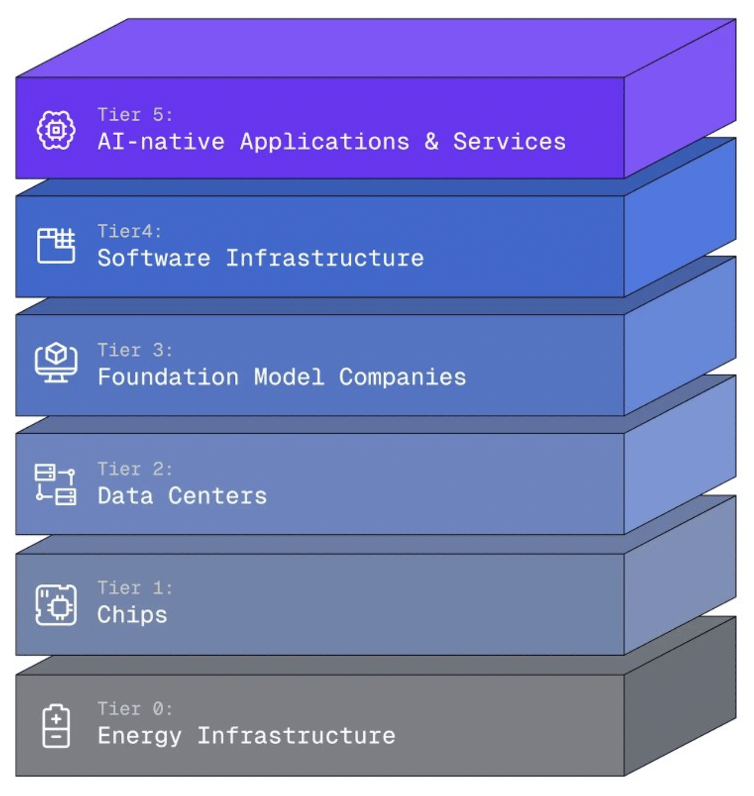

Image: Palantir founder Joe Lonsdale recently shared a framework that maps how the AI economy is structured, and it’s a useful lens for any investor trying to figure out where value accretes.

Chart: According to Boston Consulting Group, data centres’ share of US energy consumption will more than triple by 2030, and International Energy Agency (IEA) expects data centre will use more power than the entire nation of Japan (reaching approximately 945–1,000 terawatt-hours (TWh, versus 903 TWh for Japan). Other studies have suggested that by 2035, AI data centres could consume up to 1,600 TWh, which would be roughly equivalent to the total electricity consumption of India.

The risk register

This is not a one-way trade.

The Situational Awareness fund’s reported AUM as of February 2026 was US$383 million, while the 13F filing showed US$5.52 billion in gross long exposure. The 13F is not AUM. It reports long positions only and does not disclose shorts. The fund has a large gross book and is reportedly substantially leveraged.

Hyperscaler capex now sits at 2.2% of US GDP. The five hyperscalers planned to add about US$2 trillion of AI-related assets to their balance sheets by 2030, with annual depreciation expense projected at US$400 billion, more than their combined profits in 2025. Big tech companies issued US$100 billion of bonds in 2026 to fund AI capex, with investors demanding record protection via Credit Default Swaps. If revenue from AI deployment fails to scale into the depreciation curve, the entire infrastructure trade resets. The downstream effect on resource demand would be material.

The thesis is not bulletproof. But the capital is moving, the demand signals are real, and the constraint is increasingly physical rather than financial. ASX-listed companies with genuine exposure to the energy and critical minerals required to fuel the buildout sit in a position most global capital cannot replicate.

Final word

A 24-year-old running a hedge fund that beats the S&P 500 by 47% in its first six months is a story. The story behind the story is more important. Aschenbrenner’s portfolio is a public, disclosed, real-time map of where one of the most informed people in AI thinks the bottlenecks are. He has rotated out of pure chip plays and into the layer beneath them. The capital following him is doing the same.

For ASX-listed companies operating in copper, uranium, gas, rare earths, and grid-supporting critical minerals, the implication is not subtle. The global narrative around these commodities is being rewritten in real time around AI demand. The companies that articulate their exposure clearly to the right institutional audiences will compound the benefit. The companies that wait will watch capital flow past them to peers with better stories.

Most ASX miners are not telling this story clearly. Here’s what you should do:

- Reframe the equity story. Position assets explicitly as inputs into AI infrastructure, not generic commodity exposure.

- Quantify relevance. Link your project to data centre demand, electrification load, or grid support. Avoid vague “energy transition” language.

- Target the right capital. US and global funds are leading this thematic rotation. Domestic retail is not setting the marginal price.

- Tighten disclosure cadence. The market is rewarding forward-looking narrative, not backward-looking reporting.

If you are an ASX-listed company in the energy, resources, or critical minerals sector and want to position your investment narrative for the global capital flowing into AI infrastructure, get in touch via our contact page or email us directly: info@investability.com.au.

Sources

- Aschenbrenner, L. (2024). Situational Awareness: The Decade Ahead. https://situational-awareness.ai

- Fortune. Why Leopold Aschenbrenner’s AI hedge fund is betting big on power companies and Bitcoin miners to fuel the AI boom (5 March 2026). https://fortune.com/2026/03/05/leopold-aschenbrenner-ai-hedge-fund-superintelligence-agi-power-companies-crypto-miners/

- The Motley Fool. Leopold Aschenbrenner’s Situational Awareness Fund Bought Bloom Energy Stock Before a 176% Run (May 2026). https://www.fool.com/investing/2026/05/05/leopold-aschenbrenners-situational-awareness-fund/

- Linas Substack. Leopold Aschenbrenner’s $5.5B Situational Awareness Fund: Portfolio Playbook (April 2026). https://linas.substack.com/p/leopold-aschenbrenner-situational-awareness-fund-portfolio-playbook

- Capitalists Substack. Situational Awareness: The 25 Year Old Taking on Wall St (15 March 2026). https://capitalists.substack.com/p/situational-awareness-the-25-year

- Statista. Big Tech’s AI Spending to Reach $725 Billion in 2026 (May 2026). https://www.statista.com/chart/35046/capital-expenditure-of-meta-alphabet-amazon-and-microsoft/

- Tom’s Hardware. Google, Microsoft, Meta, and Amazon capex spending to hit $725 billion in 2026 (May 2026). https://www.tomshardware.com/tech-industry/big-tech/big-techs-ai-spending-plans-reach-725-billion

- Futurum. AI Capex 2026: The $690B Infrastructure Sprint (12 February 2026). https://futurumgroup.com/insights/ai-capex-2026-the-690b-infrastructure-sprint/

- Epoch AI. Hyperscaler capex has quadrupled since GPT-4’s release (26 February 2026). https://epoch.ai/data-insights/hyperscaler-capex-trend/

- Fortune. Big Tech’s $700 billion AI spending spree has no clear end (April 2026). https://fortune.com/2026/04/30/big-tech-hyperscalers-will-spend-700-billion-on-ai-infrastructure-this-year-with-no-clear-end-in-sight-eye-on-ai/

- Australian Mining. Australia poised as ‘global resource rising star’ in electrified world: IEA chief (26 March 2026). https://www.australianmining.com.au/australia-poised-as-global-resource-rising-star-in-electrified-world-iea-chief/

- Discovery Alert. AI Data Centre Copper Demand Surge: Mining Opportunities (March 2026). https://discoveryalert.com.au/copper-demand-ai-data-centres-2026/

- Livewire Markets. 7 Magnificent Miners: 2026’s top picks in copper, iron ore, lithium, rare earths, gold, silver, and uranium (February 2026). https://www.livewiremarkets.com/wires/7-magnificent-miners-2026-s-top-picks-in-copper-iron-ore-lithium-rare-earths-gold-silver-and-uranium

- Stockhead. These ASX resources stocks are aiming to hit FID in 2026 (27 February 2026). https://stockhead.com.au/resources/these-asx-resources-stocks-are-aiming-to-hit-fid-in-2026/

- IEEE ComSoc Technology Blog. Hyperscaler capex > $600 bn in 2026 a 36% increase over 2025 (22 December 2025). https://techblog.comsoc.org/2025/12/22/hyperscaler-capex-600-bn-in-2026-a-36-increase-over-2025-while-global-spending-on-cloud-infrastructure-services-skyrockets/